Page 17 - 20190415_LandAdvocacy_EN

P. 17

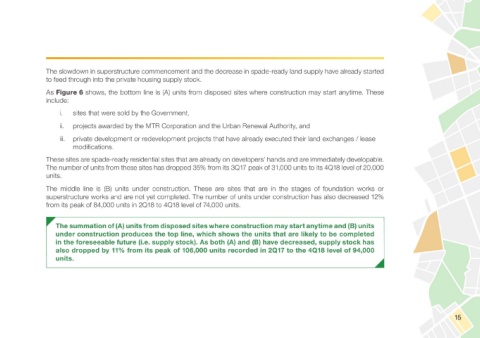

The slowdown in superstructure commencement and the decrease in spade-ready land supply have already started

to feed through into the private housing supply stock.

As Figure 6 shows, the bottom line is (A) units from disposed sites where construction may start anytime. These

include:

i. sites that were sold by the Government,

ii. projects awarded by the MTR Corporation and the Urban Renewal Authority, and

iii. private development or redevelopment projects that have already executed their land exchanges / lease

modifications.

These sites are spade-ready residential sites that are already on developers’ hands and are immediately developable.

The number of units from these sites has dropped 35% from its 3Q17 peak of 31,000 units to its 4Q18 level of 20,000

units.

The middle line is (B) units under construction. These are sites that are in the stages of foundation works or

superstructure works and are not yet completed. The number of units under construction has also decreased 12%

from its peak of 84,000 units in 2Q18 to 4Q18 level of 74,000 units.

The summation of (A) units from disposed sites where construction may start anytime and (B) units

under construction produces the top line, which shows the units that are likely to be completed

in the foreseeable future (i.e. supply stock). As both (A) and (B) have decreased, supply stock has

also dropped by 11% from its peak of 106,000 units recorded in 2Q17 to the 4Q18 level of 94,000

units.

15