Page 15 - ENGLISH_Land

P. 15

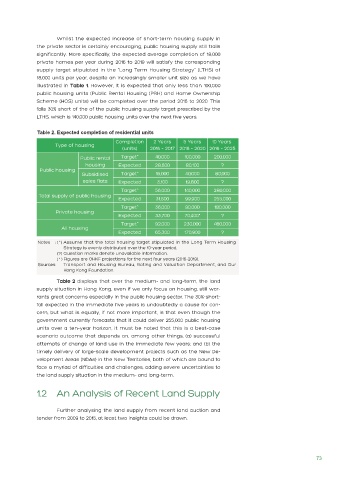

Whilst the expected increase of short-term housing supply in

the private sector is certainly encouraging, public housing supply still trails

significantly. More specifically, the expected average completion of 18,000

private homes per year during 2016 to 2019 will satisfy the corresponding

supply target stipulated in the “Long Term Housing Strategy” (LTHS) of

18,000 units per year, despite an increasingly smaller unit size as we have

illustrated in Table 1. However, it is expected that only less than 100,000

public housing units (Public Rental Housing (PRH) and Home Ownership

Scheme (HOS) units) will be completed over the period 2016 to 2020. This

falls 30% short of the of the public housing supply target prescribed by the

LTHS, which is 140,000 public housing units over the next five years.

Table 2. Expected completion of residential units

Notes : ( ^ ) Assume that the total housing target stipulated in the Long Term Housing

Strategy is evenly distributed over the 10-year period.

(?) Question marks denote unavailable information.

( * ) Figures are OHKF projections for the next four years (2016-2019).

Sources: Transport and Housing Bureau, Rating and Valuation Department, and Our

Hong Kong Foundation.

Table 2 displays that over the medium- and long-term, the land

supply situation in Hong Kong, even if we only focus on housing, still war-

rants great concerns especially in the public housing sector. The 30%-short-

fall expected in the immediate five years is undoubtedly a cause for con-

cern, but what is equally, if not more important, is that even though the

government currently forecasts that it could deliver 255,000 public housing

units over a ten-year horizon, it must be noted that this is a best-case

scenario outcome that depends on, among other things, (a) successful

attempts of change of land use in the immediate few years; and (b) the

timely delivery of large-scale development projects such as the New De-

velopment Areas (NDAs) in the New Territories, both of which are bound to

face a myriad of difficulties and challenges, adding severe uncertainties to

the land supply situation in the medium- and long-term.

1.2 An Analysis of Recent Land Supply

Further analysing the land supply from recent land auction and

tender from 2009 to 2015, at least two insights could be drawn.

73