Page 71 - ENGLISH_FullText

P. 71

collecting and compiling public information from the BD, Lands Department

(LandsD), and Town Planning Board (TPB); analysing projects held by

different developers and conducting site inspection when necessary to

determine actual construction progress. To the knowledge of the research

team, this is the first set of such statistics available free of charge in the

public domain.

The expected increase in completion of private homes echoes

with the similar rising trends in residential land supply, commencement of

housing construction and pre-sale consent approval.

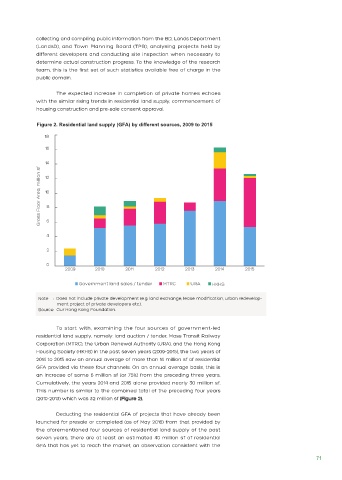

Figure 2. Residential land supply (GFA) by different sources, 2009 to 2015

Note : Does not include private development (e.g. land exchange, lease modification, urban redevelop-

ment project of private developers etc.).

Source: Our Hong Kong Foundation.

To start with, examining the four sources of government-led

residential land supply, namely: land auction / tender, Mass Transit Railway

Corporation (MTRC), the Urban Renewal Authority (URA), and the Hong Kong

Housing Society (HKHS) in the past seven years (2009-2015), the two years of

2014 to 2015 saw an annual average of more than 14 million sf of residential

GFA provided via these four channels. On an annual average basis, this is

an increase of some 6 million sf (or 75%) from the preceding three years.

Cumulatively, the years 2014 and 2015 alone provided nearly 30 million sf.

This number is similar to the combined total of the preceding four years

(2010-2013) which was 32 million sf (Figure 2).

Deducting the residential GFA of projects that have already been

launched for presale or completed (as of May 2016) from that provided by

the aforementioned four sources of residential land supply of the past

seven years, there are at least an estimated 40 million sf of residential

GFA that has yet to reach the market, an observation consistent with the

71